This update marks a significant strategic shift for Pi Network — moving toward a more mature, compliant, and possibly commercialized infrastructure. Whether this turns into a game-changing move or a user-exodus trigger depends on how the team balances user trust with regulatory ambitions.

In-Depth Analysis & Potential Implications

1. Breakdown of Core Update

-

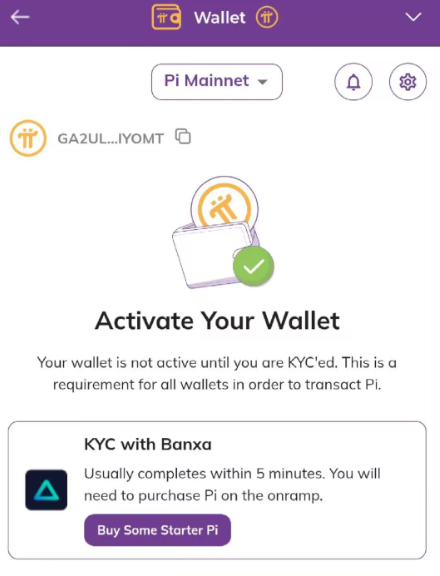

Mandatory KYC for Wallet Activation

Users are now required to complete identity verification (KYC) to access full wallet functionalities. This enhances regulatory compliance but compromises user anonymity. -

Integration of Banxa for Fast-Track KYC

Collaboration with third-party KYC provider @BanxaOfficial simplifies the process to under 5 minutes. However, it may raise concerns over data sharing and privacy. -

Starter Pi Purchase Mechanism

Users may need to purchase a “Starter Pi” to activate the wallet — a possible attempt to filter genuine users via micro-payments. -

Mainnet Migration Thresholds

Users must complete a checklist (e.g., identity linking, security verifications) to transfer mined Pi to the mainnet, effectively slowing token circulation.

2. Underlying Motivations & Strategic Intentions

2.1 Regulatory Compliance Drive

-

Responding to Regulatory Pressures

The enforced KYC aligns with growing global crypto regulations (e.g., FATF Travel Rule), preparing Pi for potential listings on major exchanges. -

Potential Data Monetization

With over 45 million users, verified identity data may become a valuable asset — potentially offered to financial institutions or advertisers in the future.

2.2 Selling Pressure Control

-

Delayed Token Release

By making mainnet migration complex, Pi can delay mass sell-offs by early miners, protecting the Pi token price in early phases. -

“Sunk Cost” Mechanism via Starter Pi

Users are nudged into making upfront purchases, increasing their commitment and reducing the likelihood of exit.

2.3 Ecosystem Consolidation

-

Filtering for Loyal Users

Dual barriers of KYC and paid activation deter airdrop hunters and ensure higher user engagement. -

Preparing for DApp Ecosystem

With full wallet functionality, Pi may soon support payments, lending, and other applications — enabling real-world utility.

3. User Risks & Challenges

-

Privacy Breach Risks

As a third-party provider, Banxa could be vulnerable to data leaks or misuse — either from hackers or internal threats. -

Rising Financial Barriers

Requiring fiat payments (e.g., $100 for Starter Pi) could exclude users from developing regions. -

Technical Complexity

Mainnet migration involves detailed procedures that may be confusing for non-technical users, potentially leading to token loss or wallet lockouts.

4. Long-Term Impact on Pi Ecosystem

Positive Outlook

-

Increased Legitimacy

Regulatory alignment and KYC might attract institutional investors and enable exchange listings (e.g., Coinbase). -

Developer Confidence

A verified user base may attract developers to build on the Pi blockchain, boosting adoption.

Potential Drawbacks

-

Centralization Concerns

Forced KYC and asset control could spark backlash from the community and node operators. -

User Attrition

If migration delays or Starter Pi costs are too high, users may shift to more accessible competitors (e.g., Sidra Bank).

5. User Action Plan

🔹 Short-Term

-

Evaluate Privacy Preferences

If you’re unwilling to undergo KYC, be prepared for restricted access — or consider exiting the ecosystem. -

Be Cautious with Payments

Only purchase Starter Pi via official channels. Avoid unverified third-party transactions.

🔹 Long-Term

-

Participate in Governance

Use node voting mechanisms to push for transparency on KYC data usage and privacy protection. -

Diversify Token Storage

Post-migration, consider moving part of your Pi holdings to hardware wallets to reduce reliance on a single platform.

© Copyright notes

The copyright of the article belongs to the author, please do not reprint without permission.

Related posts